The European renewable energy market is entering a new phase. While the number of solar and wind power facilities built has been the key indicator of the energy transition in recent years, the ability of these facilities to operate within an overloaded and volatile power grid is now playing an increasingly important role. Against this backdrop, hybrid renewable energy projects – typically co-located solar or wind generation combined with battery storage – are becoming one of the fastest-growing segments of the European energy market.

EUROPE’S CLEAN ENERGY BOOM REACHES A TURNING POINT

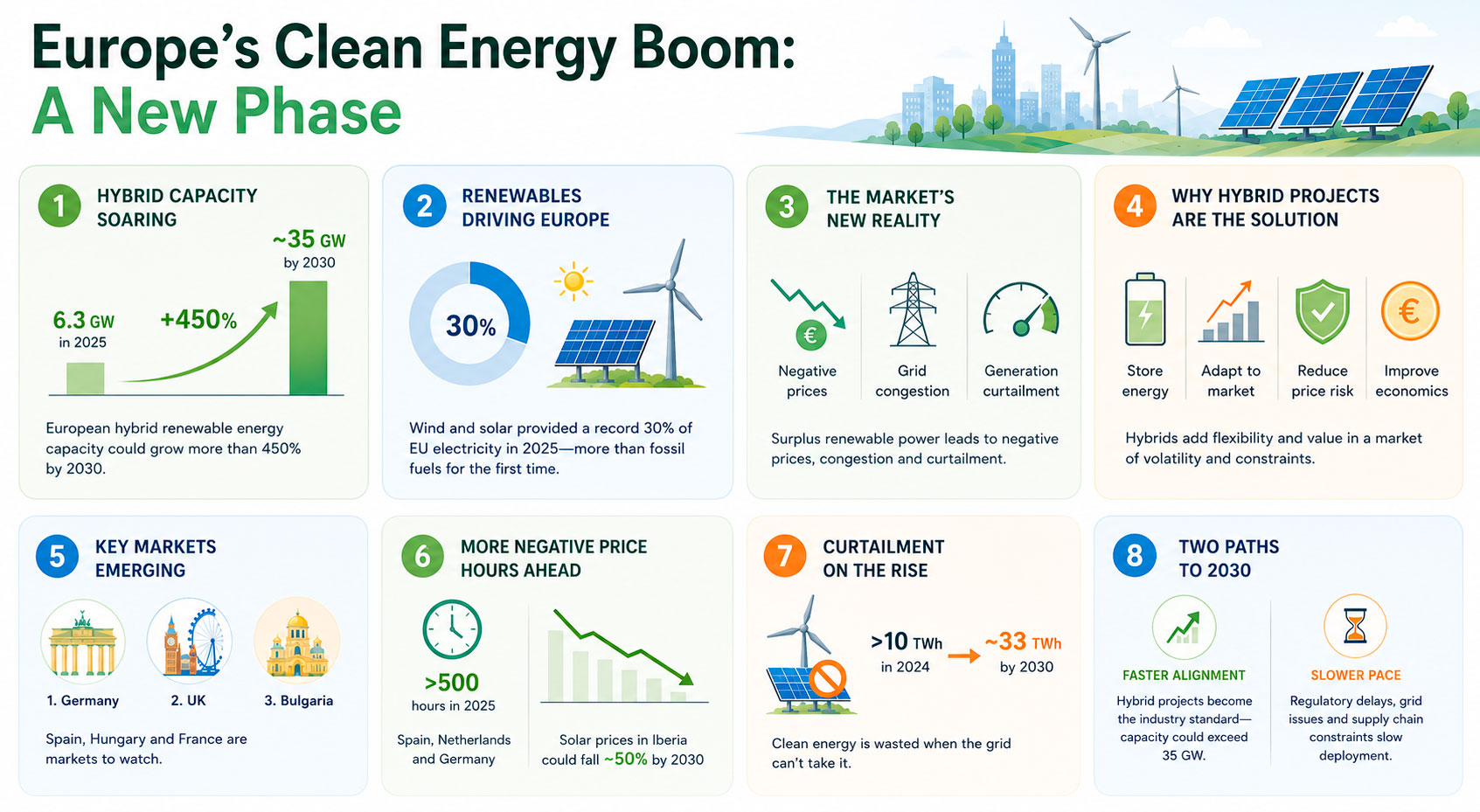

According to a report by Aurora Energy Research, the capacity of European hybrid renewable energy projects could grow by more than 450% by 2030. In 2025, it reached 6.3 GW, and by the end of the decade it is expected to increase to approximately 35 GW.

This figure is significant not only as an indicator of growth in a specific segment. It shows that Europe is moving from the first phase of the energy transition – where rapid construction of renewable energy sources was the priority – to the second phase, where integration becomes the key issue. Solar and wind generation are becoming the backbone of the energy system and are changing the rules of the market.

The main driver of hybrid projects is the rapid expansion of solar and wind energy in Europe. In 2025, wind and solar provided a record 30% of the EU’s electricity and, for the first time, generated more power than fossil fuel plants. Solar energy is growing particularly fast: its generation in the EU reached a record 369 TWh, 20% more than the previous year.

For Europe, this means reduced dependence on hydrocarbon imports, stronger energy security and progress toward climate goals. But the rapid growth of renewable energy also creates a new problem: during periods of strong wind or bright sunshine, production surges, while demand and the grid do not always keep pace.

As a result, the market is increasingly facing negative prices, grid congestion and forced curtailment of generation. This is precisely why hybrid projects are becoming a key solution for the next stage of the energy transition. They allow renewable energy projects to adapt better to market conditions, reduce the risk of falling prices and operate more efficiently in a system where surplus low-cost renewable electricity is becoming a structural feature of the market.

According to Aurora Energy Research, solar projects accounted for more than 60% of new hybrid project deployments. This makes sense: solar generation is most often concentrated during the same hours, especially in the middle of the day. If demand during these hours is not high enough and the grid cannot absorb the full volume of electricity, prices drop rapidly.

By 2030, the capacity of such projects could grow to approximately 35 GW. This trajectory suggests that developers and investors are already responding to the new market reality. For them, it is important not only to build capacity, but also to ensure the project’s economic sustainability amid price volatility and grid constraints.

Aurora outlines two possible scenarios. With faster alignment of policies and market rules, hybrid projects could become the industry standard, and their capacity could exceed 35 GW. In a slower-paced scenario, regulatory delays, grid connection issues and supply chain constraints could slow deployment.

GERMANY EMERGES AS EUROPE’S KEY HYBRID RENEWABLES MARKET

Aurora named Germany the most attractive market for hybrid projects. The main reason is the higher expected return on investment. Germany is followed by the UK and Bulgaria. Spain, Hungary and France are cited as markets to watch amid ongoing regulatory reforms.

Germany’s leadership reflects a broader shift in the European energy sector, as it effectively acts as a stress test for high-renewables system integration under real market conditions. The country is actively expanding solar and wind generation, but at the same time faces grid congestion and high price sensitivity to weather conditions. All of this makes hybrid models particularly attractive.

The UK remains one of the key markets thanks to its developed energy market structure, investor interest and the large volume of projects awaiting connection. Bulgaria demonstrates that new opportunities are emerging not only in Europe’s largest economies.

Spain has already become one of Europe’s largest solar energy markets, but for this very reason it faces price pressure during peak generation hours. France is revising its regulations amid the significant role of nuclear generation. Hungary could benefit from the growth of solar projects if it resolves grid infrastructure issues.

One of the most noticeable signs of the new market reality is the increase in the number of hours with negative electricity prices. According to Aurora, in 2025, Spain, the Netherlands and Germany each recorded more than 500 such hours. This means that during certain periods, there was more electricity in the system than the market could absorb at a positive price.

For consumers, negative prices may appear to be a sign of an abundance of cheap energy. For renewable energy producers, the situation is much more complex. If a power plant generates a lot of electricity precisely during the hours when prices drop to zero or turn negative, its average revenue price decreases. This affects the project’s return on investment.

Aurora forecasts that prices for solar generation in Iberia could fall by nearly 50% by 2030. In Germany, discounts for onshore wind power could exceed 25%. This does not mean that solar and wind power are losing their appeal. But their economics are becoming more complex: the market no longer rewards the mere fact of producing clean electricity. What matters more and more is when and where this electricity enters the grid.

Europe’s Clean Energy Shift. Graphic by the Energy Europe Editorial Team

WHEN CLEAN POWER HAS NOWHERE TO GO

Another important indicator is curtailment. This refers to situations where the output of renewable power plants is reduced to protect the power grid if supply exceeds demand or the grid cannot accept the full volume of electricity.

According to Aurora’s estimates, curtailed generation in key European markets will rise from more than 10 TWh in 2024 to approximately 33 TWh by 2030. This refers to clean electricity that could be used, but the grid is not always capable of accepting it. For investors, curtailment is becoming a risk factor: the more often a project faces curtailment, the more potential electricity goes unmonetized, which can also feed into financing costs and risk premiums.

Aurora Energy Research senior analyst Sameer Hussain put the problem bluntly: “As renewable penetration accelerates, grid congestion, curtailment and price volatility are becoming defining features of Europe’s power markets. Co-location is no longer a niche solution: it is becoming increasingly critical to protecting project economics and sustaining investment momentum.” Aurora’s forecast fits into a broader context. According to the International Energy Agency, the European Union will add more than 400 GW of new renewable energy capacity between 2026 and 2030, with solar power accounting for about 70% of this growth. Wind power will also grow rapidly and could become the largest source of electricity in the EU during the forecast period.

By 2030, the share of renewable energy in the EU’s electricity generation could reach 63%, up from 48% in 2025. The share of variable renewable energy sources – solar and wind – will rise from 30% in 2025 to 46% in 2030. This means that nearly half of Europe’s electricity will depend on weather conditions.

This is precisely why the International Energy Agency links the growth of weather-dependent generation to the need for a more flexible power system. “The strong growth of weather-dependent variable renewable energies and their rising share in many power systems during our forecast period further underscores the importance of system flexibility. Accompanying these technologies with flexible supply, storage and demand response, as well as interconnections where possible, will be crucial for their cost-effective system integration.”

EUROPE NEEDS FLEXIBLE GREEN POWER

Such a transition requires a new logic for managing the power system. The question is no longer just how many solar panels and wind turbines will be installed. The question is whether the system will be able to accept this electricity, deliver it to consumers and avoid excessive losses.

The growth of hybrid projects by more than 450% by 2030 shows that the market is beginning to respond to this challenge. Europe is entering a phase where a successful renewable energy project must be not only clean and cheap, but also flexible, manageable and resilient to price volatility.

If grids, regulation and market rules evolve rapidly, hybrid projects could become the standard for Europe’s new energy sector. Otherwise, Europe risks an energy transition paradox: there will be more renewable electricity, but an increasing portion of it will have to be curtailed, sold at low prices or lost due to system weaknesses.