Middle East turbulence is pushing European gas prices toward a new stress point and reviving a taboo question: could the EU turn back to cheap Russian energy? While Brussels vows to phase out Russian gas by 2027, the real battle is not only about inflation – it is whether Europe can resist trading long-term geopolitical security for temporary financial relief.

The escalation of the crisis in the Middle East and rising energy prices have renewed calls among some European politicians to reconsider purchases of Russian oil and gas. In particular, Hungarian leader Péter Magyar has suggested that, once the war ends, the European Union could return to buying Russian gas because it is cheaper and, in his view, dictated by competition and geography.

However, even under serious economic pressure, such a move would mean a retreat from the EU’s strategy of energy independence and a disregard for long-term risks. As long as these risks remain, a return to dependence on Russian energy cannot be seen as a sustainable solution. Short-term price difficulties should not override the long-term goals of energy security.

Geopolitical risk remains the main argument

Dependence on Russian energy is not only an economic problem but also a political one. It creates leverage that can be used in periods of geopolitical instability. Even temporary contracts with Russia would create vulnerability not only for individual countries but for the European Union as a whole.

This is why Brussels treats the phase-out of Russian energy not as a temporary response to the war but as a strategic shift. European Commission President Ursula von der Leyen has stated that the EU is set to permanently decouple from Russian fossil fuels and stressed that Europe has already taken major steps toward strategic independence. “From defense to energy, we have made the impossible possible as part of our new reality… This is Europe’s independence moment,” she said.

Returning to the old supply model would undermine confidence in the EU’s long-term policy and create the impression that the bloc is ready to sacrifice its principles for short-term gain. The question is not only about gas prices but about the kind of energy model Europe wants to build.

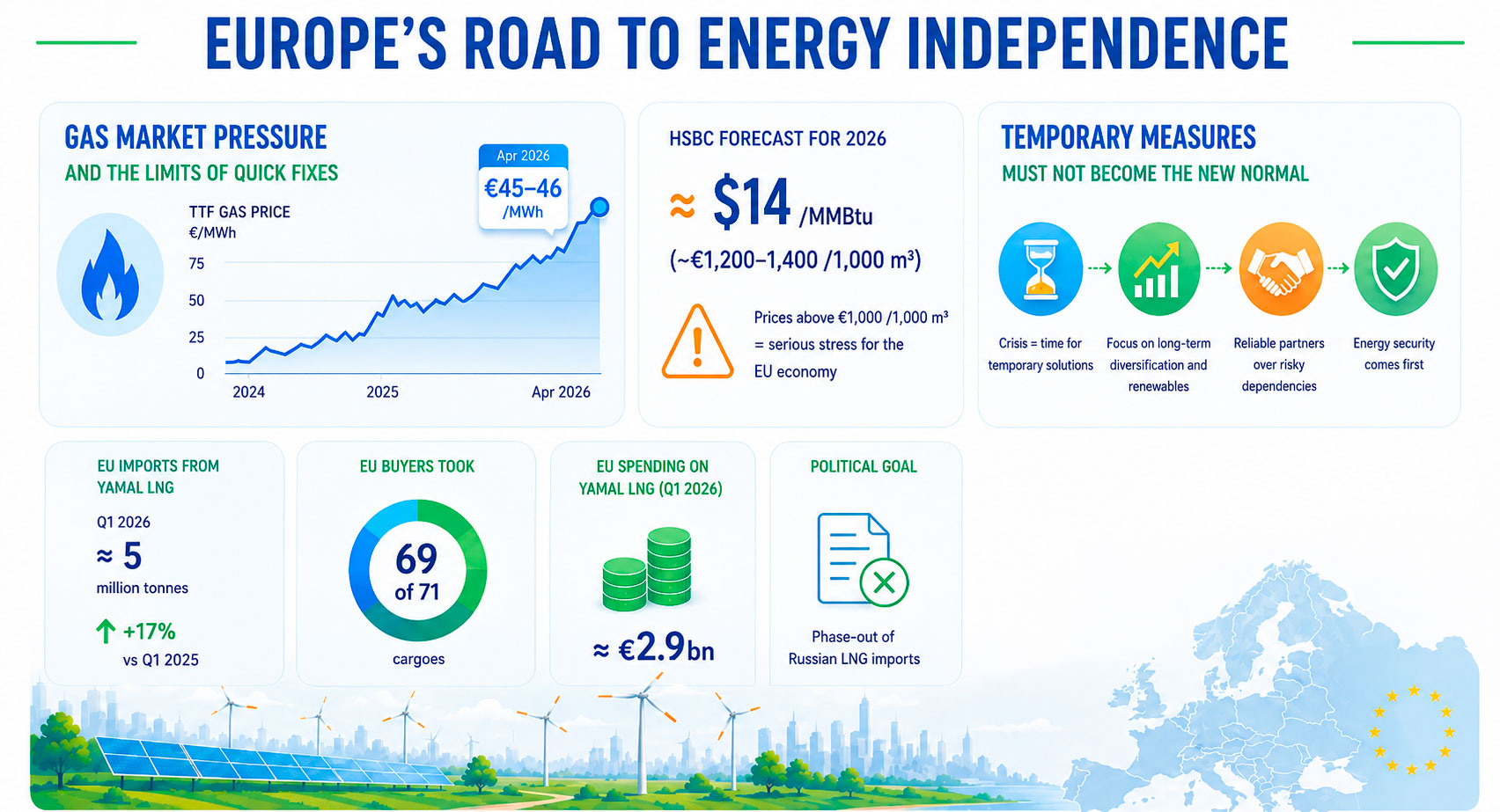

Gas market pressure and the limits of quick fixes

The Middle East crisis is dangerous for Europe not only because of the risk of physical shortages but also because of pressure on gas prices. Oil markets may, in theory, be partly stabilised through the release of strategic reserves. Gas is more complicated: without secure LNG exports from Qatar, stabilising European prices would be much more difficult.

This risk is particularly acute because Europe no longer has the same access to Russian pipeline gas as before. As of 9-10 April 2026, the spot price at the European TTF hub stood at around €45-46/MWh, equivalent to roughly €500 per thousand cubic metres. In the event of a more severe LNG shortage and continued geopolitical instability, prices could rise much further.

HSBC analysts have forecast that European gas prices in 2026 could be about 40% higher than previously expected, reaching around $14/MMBtu. Depending on exchange rates and conversion assumptions, this would be broadly comparable to around €1,200-1,400 per thousand cubic metres. Such estimates show how quickly Europe’s gas market could come under pressure if LNG supply tightens.

Prices above roughly €1,000 per thousand cubic metres are viewed by many analysts as a serious stress level for Germany and the EU economy as a whole.

Russian LNG as a symptom, not a solution

Against this backdrop, European companies continue to buy Russian LNG despite the EU’s political commitment to end such imports. The Financial Times reports that in the first quarter of 2026, imports from Russia’s Yamal LNG project to the EU rose by about 17% year on year, reaching roughly 5 million tonnes. According to the newspaper, European buyers took 69 out of 71 cargoes shipped from the project in the first three months of the year.

This example shows the contradiction between the EU’s political goal and market reality. Brussels is moving toward a ban on Russian LNG imports, yet in the short term European companies are still buying significant volumes. Campaign group Urgewald estimated that EU countries spent around €2.9bn on Yamal LNG in the first quarter.

This does not prove that returning to Russian energy is a solution. Rather, it shows how vulnerable Europe’s energy system remains in a situation of limited flexibility, competition for LNG and exposure to geopolitical shocks. Even if Russian supplies temporarily ease price pressure, they do not address the fundamental problem – the instability of the energy supply architecture itself.

In other words, this is not a return to previous stability but the risk of replacing one dependency with another. For the EU, the main task is not to find the cheapest short-term source of fuel but to build a system capable of withstanding prolonged crises without politically dangerous compromises.

Temporary measures must not become the new normal

Some experts argue that, in an acute crisis, limited and temporary purchases of Russian LNG could be considered an emergency measure to stabilise the market. But this logic is only acceptable if it does not imply a revision of the EU’s strategic course and if it is treated strictly as a short-term tool to buy time for deeper reforms.

The danger is that temporary solutions can easily turn into routine practice. If a return to Russian energy starts to be seen as a normal alternative to diversification, it will weaken incentives to develop infrastructure, renewable energy and long-term partnerships with reliable suppliers.

In December 2025, EU Energy Commissioner Dan Jørgensen told Euronews that the EU should not return to Russian gas even after peace is reached between Russia and Ukraine. “Even when there’s peace, we won’t buy Russian gas again,” he said. “We should never repeat the mistake of becoming dependent on Russian gas again.”

This approach reflects the core logic of European energy policy: a peace agreement alone does not eliminate the strategic risks of dependence. Even after the war ends, the EU’s energy security will depend on whether the bloc can avoid returning to the old model. The EU has proposed a plan to phase out Russian gas and oil imports by the end of 2027, making the legal and regulatory framework increasingly incompatible with renewed dependence.

Europe’s road to energy independence. Graphic by Energy Europe Editorial Team

The Middle East and competition for LNG

Restoring energy infrastructure in the Middle East may take time, and the exact timeline for stabilisation remains uncertain. But this pause should not become a reason to revise the EU’s strategic course. On the contrary, it underlines the need to accelerate diversification.

Intense competition between European and Asian markets for LNG will push prices upward regardless of whether Europe temporarily buys additional volumes from Russia. HSBC expects elevated gas prices linked to geopolitical risks to persist through 2027, independent of any short-term Russian supplies. In such conditions, returning to Russian energy does not solve the problem but merely delays the need for systemic decisions.

For the EU, the priority should remain the expansion of LNG import infrastructure, growth of renewable energy capacity, development of storage, greater energy efficiency and stronger ties with reliable partners outside Russia. This approach allows the Middle East crisis to be seen not as an argument for returning to old dependencies but as another confirmation of the need for diversification.

Economic pressure as a stimulus for reform

The crisis is indeed hitting the European economy. Higher energy prices increase industrial costs, raise expenses for farmers and put pressure on households. Energy-intensive sectors, including chemicals, metals and fertiliser production, remain particularly vulnerable.

However, these difficulties should become a catalyst for accelerating the transition to energy independence. Attempts to ease the current crisis through a return to Russian supplies can only be justified as a strictly limited short-term measure. If such a step begins to be perceived as an alternative to reform, it will undermine confidence in the EU’s long-term policy and weaken incentives to build a more resilient energy system.

The EU’s strategic choice

European energy policy is now being tested for consistency. High prices and geopolitical shocks make the temptation of cheap fuel especially strong. But it is precisely in such moments that strategic decisions matter most.

Dependence on a single supplier limits room for manoeuvre and creates long-term vulnerability. The EU’s goal should therefore not be a return to old schemes but the creation of a more resilient energy supply model – with expanded LNG infrastructure, a larger share of renewables, more flexible markets, energy storage and partnerships with reliable suppliers.

Short-term economic difficulties do not cancel the long-term goal of energy security. On the contrary, they show why this goal remains necessary. For Europe, the choice today is not only between expensive and cheap fuel but between temporary relief and strategic independence.