OPEC+ remains the key coordination mechanism in the global oil market, but its influence no longer seems assured. Disputes over quotas, diverging interests among participants and rising production outside the alliance are gradually changing the rules under which OPEC+ operates. The question is increasingly not whether OPEC+ will formally survive, but how much control it can still exert over the market.

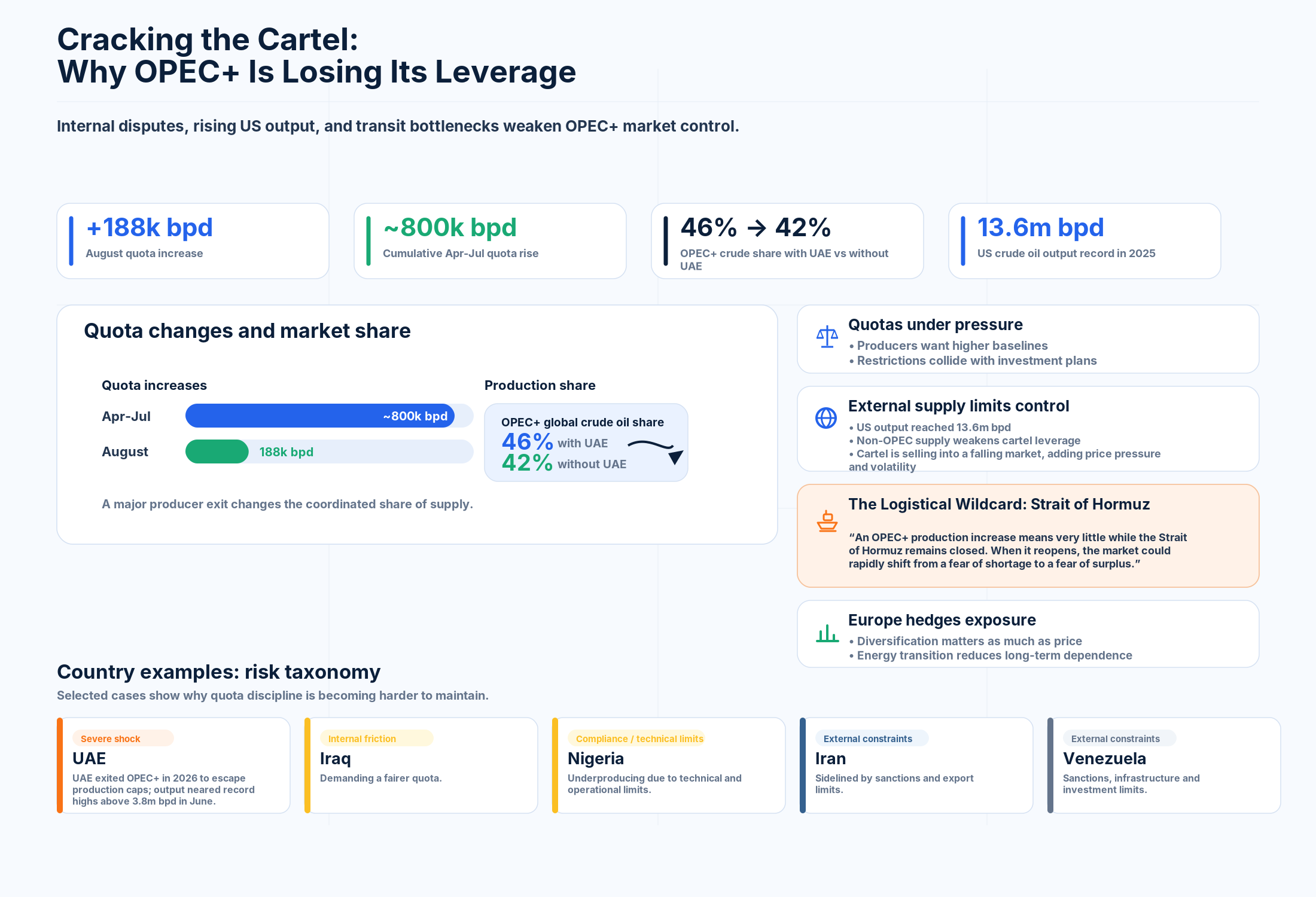

The trigger for a new debate about the future of OPEC+ was the alliance’s decision to increase production quotas in the summer of 2026. From August, they will rise by a further 188,000 barrels per day – following similar steps in June and July. Overall, between April and July, the seven key participants in the OPEC+ format had already increased their quotas by almost 800,000 barrels per day.

Formally, this demonstrates that the coordination mechanism is still working. In practice, however, quota coordination is increasingly turning into a bargaining process between countries with different priorities: for some, it is a tool for supporting prices; for others, a constraint that prevents them from increasing exports and recouping investments.

The broader the format, the harder it becomes to maintain discipline. OPEC+ brings together not only members of the cartel but also external producers, including Russia and Kazakhstan – and this is precisely what makes decision-making more fragile. According to the EIA, even the exit of one major player reduces the alliance’s share of global production from around 46% to 42%. This shows how sensitive the system remains to the decisions of individual major producers.

Quota revisions and the battle for market share

The main source of tension within OPEC is the production quota system. For countries that prioritise price support, restrictions help keep the market from becoming oversupplied. For countries that have invested in expanding production or urgently need budget revenues, those same restrictions become a problem.

The most visible example is the UAE. Abu Dhabi had been pushing for several years to revise its baseline production level, citing large-scale investments in expanding production capacity. On 28 April 2026, the UAE announced that it would leave OPEC and the broader OPEC+ format, with the decision taking effect on 1 May. The dispute then moved into a tougher phase: the UAE pushed production to near-record levels of over 3.8 million barrels per day in June 2026.

Wood Mackenzie explains this step precisely through the conflict between the UAE’s growing capacity and the alliance’s restrictions: “OPEC+ quotas, however, have constrained output well below capacity, to the UAE’s growing frustration.”

This case matters not only in its own right. It shows that, for major producers, quotas can become a strategic issue rather than a technical one. If a country invests in production but cannot use new capacity because of alliance restrictions, a dispute over limits can turn into a question of participation in OPEC+.

Iraq is another important example. It is OPEC’s second-largest producer after Saudi Arabia and one of the organisation’s founding members. For Baghdad, higher production is primarily linked to the need to increase export revenues, support the budget and attract investment into the oil sector. At the same time, Iraq is not talking about an immediate exit. Experts agree that Iraq will not leave OPEC, but will continue to push for a fair production quota.

Nigeria is in a different situation. It also needs room for production growth, but its capacity is limited not only by quotas. According to IEA data, in May 2026 Nigeria was producing around 1.47 million barrels per day, against a target of around 1.5 million barrels per day. This shows that, for the country, the issue is not only quota revision, but also its ability to produce consistently at the stated level.

Internal contradictions within OPEC+

The main line of tension within OPEC runs between countries that focus on price support and countries for which increasing production volumes is more important. Saudi Arabia has traditionally sought to manage supply cautiously in order to keep prices at a level acceptable to producers. For a number of other participants, however, export growth in the short term is more important.

The OPEC+ format makes this balance even more complicated. Russia remains one of the key participants in the expanded alliance, despite its international isolation over the war in Ukraine. However, its position is determined less by market logic than by sanctions, changes in export flows and budgetary needs. This complicates negotiations within OPEC+.

The issue of discipline is becoming particularly sensitive. Even if the alliance formally remains in place, its influence on the market depends on participants’ willingness to fulfil their commitments. If quotas begin to be perceived as too rigid or inconvenient, OPEC+’s ability to coordinate production declines.

Structural weakening of the cartel

The United States is consistently reducing the global market’s dependence on OPEC decisions. This is happening not only through policy, but also through the structure of supply itself. The US remains the world’s largest oil producer, and its output is not subject to OPEC+ discipline.

According to the EIA, US crude oil production in 2025 rose by 3%, or 350,000 barrels per day, reaching a new annual record of 13.6 million barrels per day. This limits OPEC+’s ability to influence prices solely through its own decisions: the more oil comes from sources outside the alliance, the harder it is for the cartel to manage the market.

Sanctions against Iran and Venezuela also matter. For now, they restrict these countries’ exports, but at the same time they create a delayed risk for OPEC. If sanctions are eased, additional oil could return to the market, and the issue of quota redistribution within the alliance will become even more complicated.

Europe is diversifying its oil imports

The EU’s position on OPEC is ambivalent. On the one hand, Europe needs stable oil supplies at predictable prices. On the other, the EU’s long-term policy is aimed at decarbonisation and reducing dependence on fossil fuels.

After reducing purchases of Russian energy resources, Europe has been looking more actively for alternative suppliers, including countries in the Middle East, Africa and the US. For the EU, not only prices matter, but also supply reliability, diversification of sources and alignment with climate goals.

In this sense, Europe’s approach can be called pragmatic. The EU continues to interact with oil exporters, but at the same time seeks to reduce its long-term dependence on their decisions. The further the energy transition progresses, the less Europe wants to depend on OPEC+ decisions on quotas and production.

The Iran and Venezuela factor

Iran and Venezuela occupy a special place within OPEC. Their ability to increase production is limited by sanctions and internal problems in the sector, but they could potentially change the supply balance.

Iran insists on its right to restore higher levels of production and exports. For Tehran, this is not only an economic issue, but also a political one: the country does not want the sanctions period to lock it into a weaker position in the oil hierarchy.

Venezuela is also interested in returning to the market. But sanctions are not the only problem here. The state of infrastructure, lack of investment and technological constraints remain limiting factors. Therefore, even if external pressure eases, production growth is likely to be gradual.

According to IEA data, in May 2026 Iran was producing around 2.3 million barrels per day, while Venezuela was producing around 1.08 million barrels per day. These volumes show that the return of additional supply from these countries could become an important factor for the market, but will not necessarily happen quickly.

An inside look at the structural shifts and supply risks threatening OPEC dominance. Graphic by the Energy Europe Editorial Team.

Between shortage and surplus

A full collapse of OPEC looks unlikely in the short term. For many countries, participation in the organisation still provides important advantages: a negotiating platform, political coordination and the ability to influence the global oil agenda.

A more realistic scenario is a gradual decline in controllability. OPEC may survive as an institution, but its ability to tightly coordinate production will depend on whether participants can agree on new terms for quota allocation and maintain discipline.

What matters here is not only the size of the quotas themselves, but also the physical ability to deliver oil to the market. Jorge Leon, Rystad Energy’s head of geopolitical analysis and a former OPEC official, noted: “An OPEC+ production increase means very little while the Strait of Hormuz remains closed.” He also warned: “When the Strait of Hormuz reopens, the market could move very quickly from fear of shortage to fear of surplus.”

This assessment clearly shows the double risk facing OPEC+. While logistics are disrupted, a formal quota increase may have almost no effect on actual supplies. But if routes recover quickly, the market could move from fears of shortage to expectations of oversupply.

UBS analyst Giovanni Staunovo makes a similar point. According to him, in the near term the market’s attention will be focused on how many tankers can pass through the Strait of Hormuz: “The near-term focus will remain on how many tankers will manage to cross the Strait of Hormuz and how quickly demand and Chinese crude imports recover.”

PVM analyst Tamas Varga describes the situation even more sharply: “They are selling into a falling market, offering little hope of an imminent price recovery.”

Expectations of oversupply, rising production outside the alliance and uncertainty around key participants are increasing pressure on prices. Under these conditions, it becomes harder for countries to explain to their own governments and investors why they should limit production.

What this means for Europe

If OPEC loses part of its ability to coordinate production, the oil market will become more volatile. In the short term, this could mean sharper price fluctuations, and in the long term, greater uncertainty for producers and investors.

In its June report, the International Energy Agency forecast a decline in global oil demand in 2026: “Global oil demand is forecast to decline by 1.1 mb/d y-o-y in 2026.” At the same time, the IEA expected global supply to fall to 102.4 million barrels per day in 2026, before recovering to 110.3 million barrels per day in 2027.

For Europe, the consequences will be twofold. On the one hand, increased competition could help lower prices for oil and petroleum products. On the other, rising volatility increases risks for industry, transport and energy security.

In the context of the energy transition, what matters for the EU is not only price, but also the predictability of supplies. Therefore, a weakening of OPEC’s role could benefit Europe only if it does not lead to chaotic market fluctuations.

Thus, this is not about the imminent collapse of OPEC, but about a gradual transformation of its role. The alliance is likely to retain its status as a platform for coordinating producers’ actions, but its ability to directly manage the market will increasingly depend on the balance of interests among participants and on external pressure from the largest energy consumers.