The debate over Hormuz is shifting from whether fees are acceptable to whether they could help restore predictable transit. With Europe, Gulf states and Oman exploring possible models, a once-unthinkable option is moving closer to the centre of regional diplomacy. Before the war, the Strait of Hormuz, through which around a fifth of the […]

Oil and Gas

In its quest to diversify its energy sources and strengthen its energy security, the European Union is increasingly looking south. Africa is a logical geopolitical choice: it already meets around 20 per cent of Europe’s gas needs through pipeline supplies from North Africa and LNG from Nigeria. New routes from Nigeria via Algeria and Morocco […]

Middle East turbulence is pushing European gas prices toward a new stress point and reviving a taboo question: could the EU turn back to cheap Russian energy? While Brussels vows to phase out Russian gas by 2027, the real battle is not only about inflation – it is whether Europe can resist trading long-term geopolitical […]

China initially appeared to be among the biggest potential losers from the crisis around the Strait of Hormuz. Yet Beijing’s vast oil reserves, diversified supply network and rapid electrification strategy may allow it to weather the shock far better than many experts expected. As global concerns over energy security intensify, the crisis could ultimately strengthen […]

The Strait of Hormuz is far away but a crisis there could directly affect Europe’s airports. In response, the EU has developed an emergency plan for jet fuel and is exploring ways to address a new vulnerability in its supply security. Industry warnings suggest that, if the blockade continues, shortages could arise even before the […]

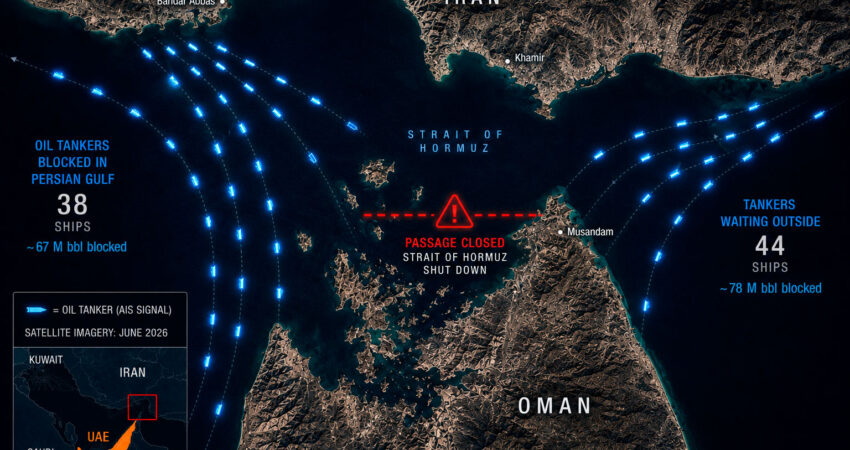

The Strait of Hormuz has once again become a source of global alarm – and this time, the issue is not only war, but also the risk of a major energy shock. Disruptions along this route could trigger a surge in oil and gas prices, drive up inflation, and hit the world’s largest economies. That […]

German Chancellor Friedrich Merz’s visit to Qatar in February 2026 was more than just a bilateral meeting. It is part of a broader European Union strategy to diversify LNG supplies. Against the backdrop of increasing dependence on American LNG and growing unpredictability in Washington, Berlin and Brussels are trying to make their energy supply more […]

As Europe moves deeper into the winter of 2025-2026, the continent’s energy system reflects a transformation shaped by cooperation, investment, and strategic foresight. Technically, electricity and gas supplies are broadly secure across the Union. Economically, markets remain sensitive to global conditions but they are now operating within a framework that is more diversified, more connected, […]

Venezuela’s recent political upheaval has triggered renewed attention in global energy markets, but oil prices remain muted, with Brent crude trading around $60 per barrel. According to analysts, this muted reaction reflects broader supply conditions rather than a lack of concern about Venezuelan instability. Political Earthquake, Limited Price Reaction The U.S. military’s operation to capture […]

For some time, Azerbaijan has been seen as one of Brussels’ allies in its efforts to diversify energy imports. However, the situation appears to have stalled, with multiple factors converging to limit the participation of Azeri gas in the European energy mix. In this article, we assess the potential of this partnership. The grand plans […]

Europe is facing new challenges in the energy sector that are fundamentally reshaping its strategy. The pivotal decision to abandon energy supplies from Russia opens the door to a deeper transatlantic partnership. The US is emerging as a confident leader in liquefied natural gas (LNG) supply and is ready to provide reliable, long-term exports. For […]