In its quest to diversify its energy sources and strengthen its energy security, the European Union is increasingly looking south. Africa is a logical geopolitical choice: it already meets around 20 per cent of Europe’s gas needs through pipeline supplies from North Africa and LNG from Nigeria. New routes from Nigeria via Algeria and Morocco could supplement these volumes in the long term. However, a significant gap remains between political ambition and engineering and economic reality.

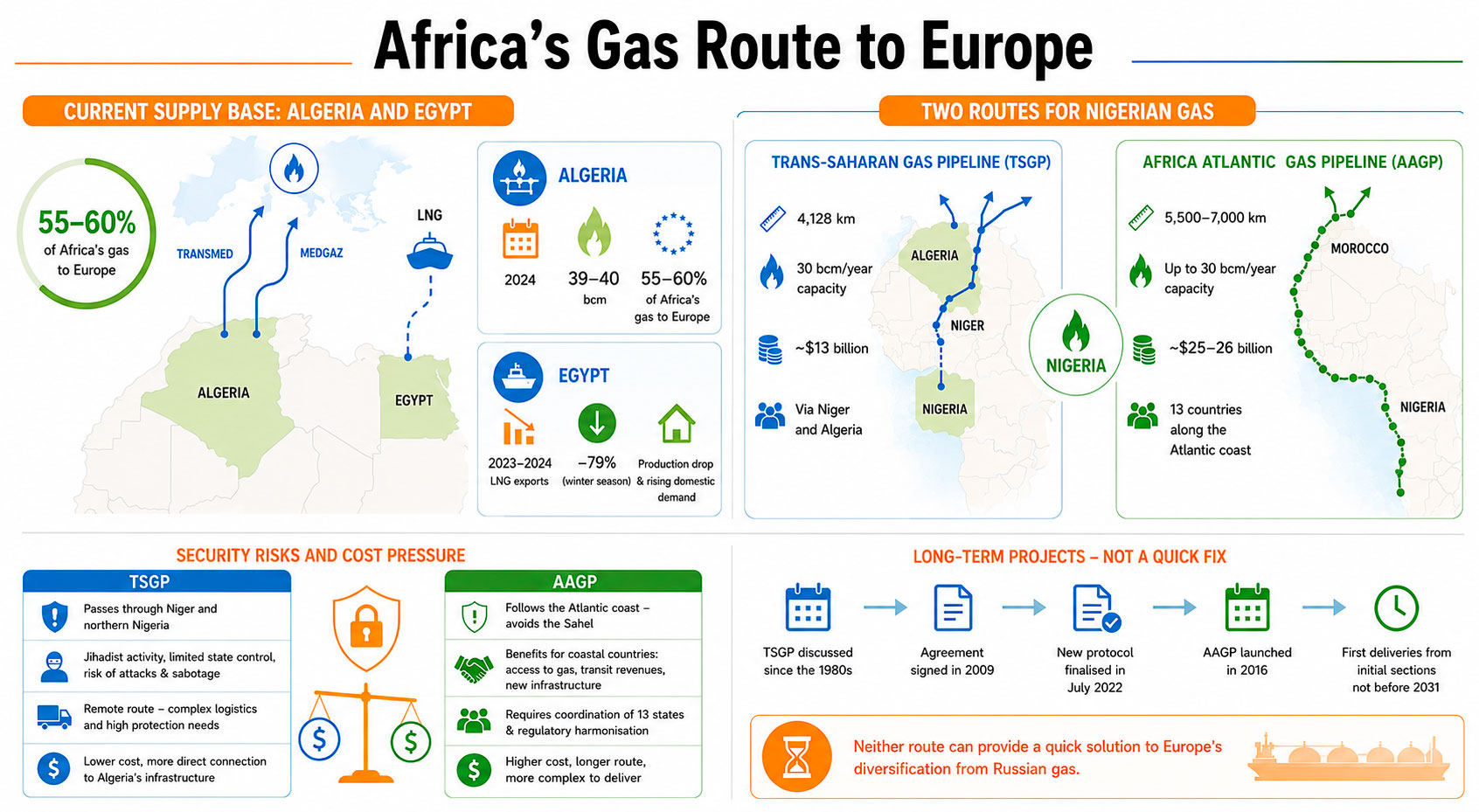

CURRENT SUPPLY BASE: ALGERIA AND EGYPT

Algeria plays a central role in Europe’s existing African gas infrastructure. In 2024, it supplied around 39-40 billion cubic metres of gas to the EU – equivalent to approximately 55–60 per cent of all African gas supplies to Europe, taking into account both pipeline gas and LNG. Since 2022, the Transmed and Medgaz routes have become key elements in replacing previous Russian volumes. For Algeria itself, the new situation has also created a commercial opportunity. Zine Labidine Ghebouli, an Algerian political scientist at the European Council on Foreign Relations, stated: “For Algiers, the 2022 [Ukraine] crisis was seen first and foremost as a commercial opportunity, but one that came with no strings attached.”

However, any long-term increase in exports will depend on investment in production and on growth in domestic consumption.

Egypt complements the African route with LNG, but its example highlights another constraint: the dependence of exports on production and domestic demand. In June 2022, the EU, Egypt and Israel signed a memorandum in Cairo on the supply of gas from the Eastern Mediterranean to Europe. However, between 2023 and 2024, Egyptian LNG exports fell sharply: during the winter season, they amounted to around 0.9 million tonnes, approximately 79 per cent less than in the previous year. The reason was a fall in production volumes and rising domestic demand for fuel.

TWO ROUTES FOR NIGERIAN GAS

A second potential source of new volumes for Europe is Nigeria, which has large natural gas reserves and is involved in two projects aimed at reaching the European market.

The Trans-Saharan Gas Pipeline (TSGP) is intended to deliver Nigerian gas to Europe via Niger and Algeria. Its planned length is 4,128 kilometres, with a planned capacity of 30 billion cubic metres per year. Once connected to the Algerian system, the gas will be able to feed into existing export routes, including Transmed, Medgaz, Maghreb-Europe and, potentially, Galsi.

The TSGP project has gained new momentum since 2022. In June, Algeria announced the start of construction on its 1,210-kilometre section. Niger plans to begin construction on its 720-kilometre section in early 2027. No start date has yet been announced for the Nigerian section. An alternative route is the African Atlantic Gas Pipeline (AAGP), also known as the Nigeria-Morocco Gas Pipeline. Its length is estimated at 5,500-7,000 kilometres, with a design capacity of up to 30 billion cubic metres per year. The pipeline is set to run along the Atlantic coast through 13 countries, including Nigeria, Benin, Togo, Ghana, Côte d’Ivoire, Liberia, Sierra Leone, Guinea, Guinea-Bissau, The Gambia, Senegal and Mauritania, before reaching Morocco and connecting to European infrastructure.

In terms of cost and infrastructure, the TSGP appears to be the more direct route. Its estimated cost is around $13 billion. The project is being led by state-owned companies from the participating countries, primarily Algeria’s Sonatrach and Nigeria’s NNPC, and the pipeline itself could be connected to existing Algerian infrastructure, including the Hassi R’Mel gas hub and export routes to Europe.

The outlook for the AAGP is less certain. The project is being led by Nigeria and Morocco, but the final financing plan for construction has not yet been announced. This route is longer, passes through 13 countries along the Atlantic coast and requires more complex intergovernmental coordination. Its cost is estimated at $25-26 billion – roughly twice that of the Trans-Saharan Gas Pipeline.

SECURITY RISKS AND COST PRESSURE

For Europe, the AAGP matters because it could expand the West African supply route without passing through the Sahel – a region where jihadist groups are active. This distinguishes it from the TSGP, which is set to pass through Niger and northern Nigeria, where construction of major energy infrastructure carries heightened security risks.

In Niger, following the 2023 coup, power is held by a military government which, according to experts, does not fully control the country’s territory. For the pipeline, this poses a risk not only at the political approval stage, but also in terms of securing construction sites, equipment, personnel, logistics corridors and future compressor stations. The remote nature of the route creates an additional vulnerability: construction across hundreds of kilometres of sparsely populated territory requires temporary camps and complex logistics for materials, fuel and equipment. Given the state’s limited control, this increases the risk of attacks, sabotage and extortion.

The AAGP shifts the route towards the Atlantic coast and therefore mitigates some of these risks. For the countries along the route, the project could provide access to gas, transit revenues and new infrastructure. “The Africa-Atlantic Gas Pipeline (AAGP), also known as the Nigeria-Morocco Gas Pipeline, is a major transcontinental infrastructure project poised to connect West African gas reserves with North African networks and European markets, potentially reshaping regional energy dynamics, boosting economic development, and enhancing energy security,” says Ayat-Allah Bouramdane, an expert at the International University of Rabat.

However, both projects remain long-term and capital-intensive. The construction of the TSGP was first discussed as far back as the 1980s; the relevant agreement between Nigeria, Algeria and Niger was signed in 2009, while a new protocol was only finalised in July 2022. The AAGP was launched in 2016, but its final phase is estimated to take place between 2035 and 2040, while Moroccan officials do not expect the first deliveries from the initial sections before 2031. Neither of the two routes can therefore provide a quick solution to Europe’s move away from Russian gas.

For the TSGP, the main constraint remains security risks in Niger and northern Nigeria. Will Brown, a Sahel expert at the European Council on Foreign Relations, believes: “It is quite difficult to imagine that Niger’s military government will be able to secure large-scale construction work across hundreds of miles in remote areas, where jihadist groups in the Sahel and neighbouring Nigeria are increasingly coordinating their actions across borders, in the near future.”

According to Brown, security risks in northern Nigeria also complicate plans to build the gas pipeline.

For the AAGP, the main constraints relate to the scale of the project, its cost and the number of participating countries. A coastal route reduces dependence on transit through Niger, but requires coordination between 13 states, the harmonisation of national regulatory regimes and the securing of long-term financing. According to Ayat-Allah Bouramdane of the International University of Rabat: “Success depends not only on sound technical design and favorable geopolitical alignment but also critically on the careful selection and prioritization of gas transit strategies that are robust, feasible, and sustainable amid future uncertainties.”

Africa’s Gas Route to Europe. Graphic by the Energy Europe Editorial Team.

GAS IN THE AGE OF THE GREEN TRANSITION

EU climate policy adds another layer of complexity. The European Union is simultaneously seeking new sources of gas while pursuing a policy of reducing its role in the energy mix through renewable generation and improved energy efficiency. “In the short to medium term, the EU overestimated how quickly partner countries could deliver more gas,” says Ugnė Keliauskaitė, an analyst at the European think tank Bruegel.

According to her, “The EU can hardly commit to stable gas imports, as its demand will keep declining due to the electrification of heating and renewable electricity generation.”

As Alberto Rizzi, an expert at the European Council on Foreign Relations, notes, gas-producing countries are competing to supply cleaner, lower-emission gas in order to secure contracts with the EU: “There’s a race between gas-producing countries to deliver slightly cleaner, lower-emission gas in order to be the one supplying the EU. But the problem is that the deadlines and current requirements the EU is putting in place are very dangerous for Algeria or Egypt, because they really struggle to meet these kinds of targets.”

Algeria has already managed to hedge against these risks: the TaqatHy+ programme being implemented in the country, jointly funded by the EU and Germany, has received around €28 million in European support. It is aimed at developing renewable energy, green hydrogen and energy efficiency, as well as reducing methane emissions and minimising gas flaring. Similar programmes could be rolled out to other countries in the region. At regional level, the EU has signed a €300 million guarantee agreement with the German development bank KfW and its subsidiary DEG to support the green transition in the Middle East and North Africa.

A LONG-TERM PARTNERSHIP, NOT A QUICK FIX

Even with the development of new routes, African gas will not bridge the entire European shortfall. According to Ayat-Allah Bouramdane’s calculations, by 2050 Europe will be able to source around 358 billion cubic metres of gas per year from non-Russian sources, but the potential annual shortfall could still amount to around 42 billion cubic metres per year. This means that the AAGP, TSGP, supplies from Algeria, Norway, the North Sea and LNG should be viewed not as one supplier replacing another, but as elements of an overall diversification strategy.

The European Union views its partnership with Africa as a long-term marathon, rather than a sprint. The strengths of this approach lie in Algeria’s existing role, Nigeria’s substantial resource base and the potential to build new pipeline links with a capacity of up to 30 billion cubic metres (bcm) per year for each of the two projects. A realistic timeframe for African gas to play a more significant role in European imports is not expected before the period 2030-2033.

For Europe, Africa is not a short-term lifeline, but a strategic choice requiring patience and systematic effort. The aim is to build a sustainable partnership framework in which environmental, social and safety standards will be as important as the volume of gas transported. Support for new projects must therefore remain prudent: the focus will be on investments that guarantee long-term reliability for all participants.