Europe’s wood pellet industry became a central part of the EU’s move away from coal, but its future is now under pressure from tougher sustainability rules, political scrutiny, and doubts about its climate benefits. As Europe tightens biomass standards after 2027, the future of wood pellets may depend on proving they are truly green.

Wood Pellets and Europe’s Energy Transition

Wood pellets occupy an increasingly controversial position in Europe’s energy transition. Classified as renewable energy, they have been widely used to replace coal in power generation and heating systems. At the same time, they face growing criticism over uncertain climate benefits and mounting pressure on European and overseas forests.

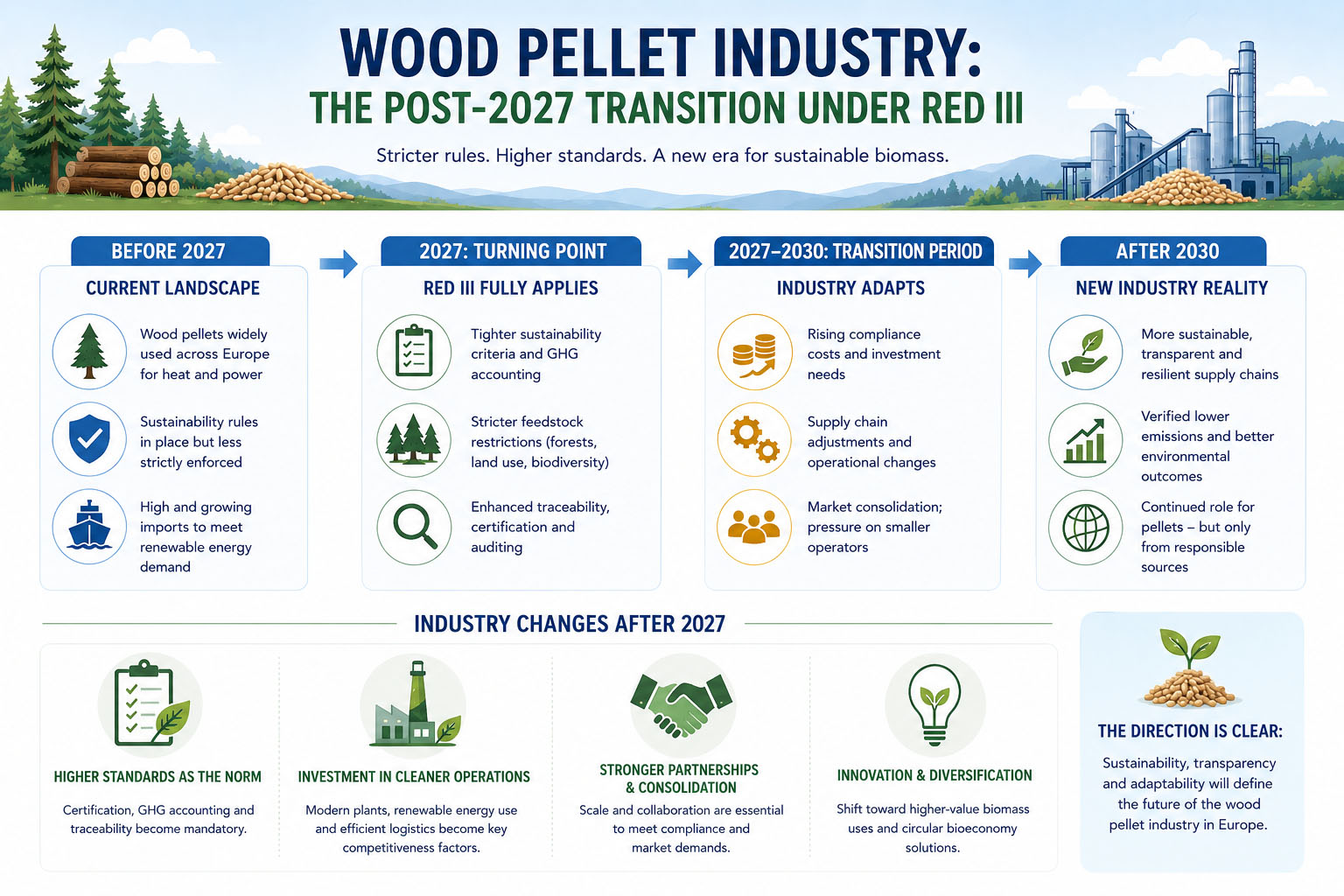

Under the EU’s revised Renewable Energy Directive (RED III), adopted in 2023, sustainability requirements for biomass are tightening significantly. Over the coming years, as the directive is transposed into national law and enforcement standards become stricter, the wood pellet sector could face serious structural risks.

Biomass plays a major role in Europe’s renewable energy system. Biomass accounts for a substantial share of renewable energy production in the EU, according to RES Foundation, though the exact share depends on how the total is measured and which year is used. Forestry biomass, especially wood pellets, represents one of the largest biomass energy sources. Wood pellets are widely used for electricity generation, but even more commonly for heating purposes.

Europe’s Growing Reliance on Wood Pellets

The EU has become the world’s largest wood pellet market, although East Asian countries such as Japan and South Korea are also rapidly increasing their consumption. European demand has grown steadily and reached 24.8 million metric tons in 2022. Part of this surge was driven by the COVID-19 pandemic, which disrupted other energy supply chains. In 2021 alone, annual demand growth reached 18%, according to Bioenergy Europe. Russia’s invasion of Ukraine and the EU’s efforts to phase out fossil fuels of Russian origin have kept demand elevated since 2022.

The economic scale of the sector is also substantial. Depending on pellet prices, Europe’s annual wood pellet market is estimated to be worth several billion euros. During the energy crisis of 2022, industrial pellet prices in Europe surged to record levels, at times exceeding €500 per metric ton in spot markets. Even at more moderate average prices, annual EU pellet consumption of nearly 25 million metric tons represents a market worth well above €5-7 billion.

Around one third of all pellets consumed in Europe are used by industry, while the remaining two thirds are consumed by households and the commercial sector.

The largest users of wood pellets in the EU are Italy, Germany, the Netherlands, Denmark, France, Sweden, Austria and Belgium. The Netherlands has also become one of Europe’s main pellet trading hubs, while the United States remains the EU’s largest external supplier. EU pellet imports remain substantial, with the U.S. continuing to dominate external supply in recent years.

The Not-So-Clean Biofuel

Since the 2010s, when wood pellets began to gain recognition as a renewable energy source, growing evidence has questioned their environmental credentials.

Critics argue that although biomass is technically renewable, its overall climate impact remains heavily debated. Peer-reviewed studies have found that CO2 emissions per unit of energy from burning wood pellets for electricity or heat can be high, and in some cases comparable to coal depending on the feedstock, technology, and accounting method used. This is partly because wood is less energy-dense than coal.

EU and IPCC accounting frameworks often classify these emissions as biogenic CO2, assuming that newly planted trees or regrowth will eventually reabsorb the carbon released at combustion. However, this carbon payback can take decades or longer, which many climate experts see as incompatible with near-term climate targets.

Critics also argue that low-grade wood waste alone is often insufficient for large-scale pellet production. As a result, forests may be logged specifically to supply pellet manufacturing facilities.

In addition, pellet production itself is energy-intensive and can expose workers to hazardous fine particles linked to respiratory illnesses and other health risks.

Why RED III Changes the Equation

Alongside raising the EU renewable energy target to at least 42.5% by 2030, RED III, introduces substantially stricter sustainability requirements for bioenergy.

The directive places greater emphasis on the protection of primary and old-growth forests, restrictions on biomass sourced from biodiversity-sensitive areas, stronger documentation and traceability standards, lifecycle greenhouse-gas accounting, and the prioritization of cascading biomass use. In practice, this means wood should first be used for materials and industrial purposes before being burned for energy.

These requirements apply to heat and power installations above 7.5 MW using solid biomass fuels, including wood pellets.

Together, the new rules could make feedstock scarcer, supply chains less predictable, and regulatory approval more difficult. The cascading-use principle may also reshape pellet economics by favoring higher-value wood applications over combustion.

Compliance requirements are expected to become stricter as well. Producers must now conduct additional risk assessments, greenhouse-gas accounting, and independent audits. Large producers may be able to absorb these costs, while smaller operators could struggle to remain competitive.

Producers unable to demonstrate transparent and compliant supply chains risk losing their renewable-energy status. That would also mean losing access to lower taxes, subsidies, and other regulatory advantages associated with renewable energy production. Without these incentives, many business models may struggle to remain economically viable.

Wood Pellet Industry in Transition. Graphic by Energy Europe Editorial Team

The Political Battle over Biomass

Beyond economics and regulation, biomass has also become an increasingly political issue.

Environmental organizations argue that existing safeguards remain insufficient to prevent deforestation and biodiversity loss. Industry groups counter that forest residues replacing fossil fuels can still deliver meaningful climate benefits. Trade unions often support the sector as a source of industrial employment and regional economic stability. Meanwhile, some academic researchers argue that current governance mechanisms remain too weak to guarantee sustainability outcomes.

At present, critics of large-scale biomass appear to be gaining influence in the European debate. Public pressure has already shaped EU discussions around the role of primary woody biomass.

At the same time, the biomass industry still occupies an important position in regions where pellet production has replaced parts of the declining coal economy, not only as an energy source but also as a major employer. This could further complicate future political negotiations around RED III implementation.

Who Will Survive?

Not all pellet producers face the same level of exposure.

Wood pellets with transparent and traceable sourcing are still regarded by many regulators and parts of the energy industry as one of the more sustainable forms of biomass fuel. This could favor large vertically integrated companies that control multiple stages of the wood supply chain.

However, the amount of available high-quality feedstock is likely to shrink under RED III.

Ultimately, RED III signals a broader shift away from volume-driven biomass expansion toward evidence-based sustainability standards. The companies that survive will likely be those capable of proving – to regulators, investors and the public – that wood pellets deliver genuine climate benefits rather than simply lower political emissions on paper.