Europe is betting billions on carbon capture technology as it races toward climate neutrality by 2050. From Norway’s offshore storage hubs to industrial CO₂ networks in Rotterdam, CCS is rapidly moving from pilot phase to strategic infrastructure – despite high costs, regulatory hurdles and growing scepticism.

A growing role in Europe’s climate strategy

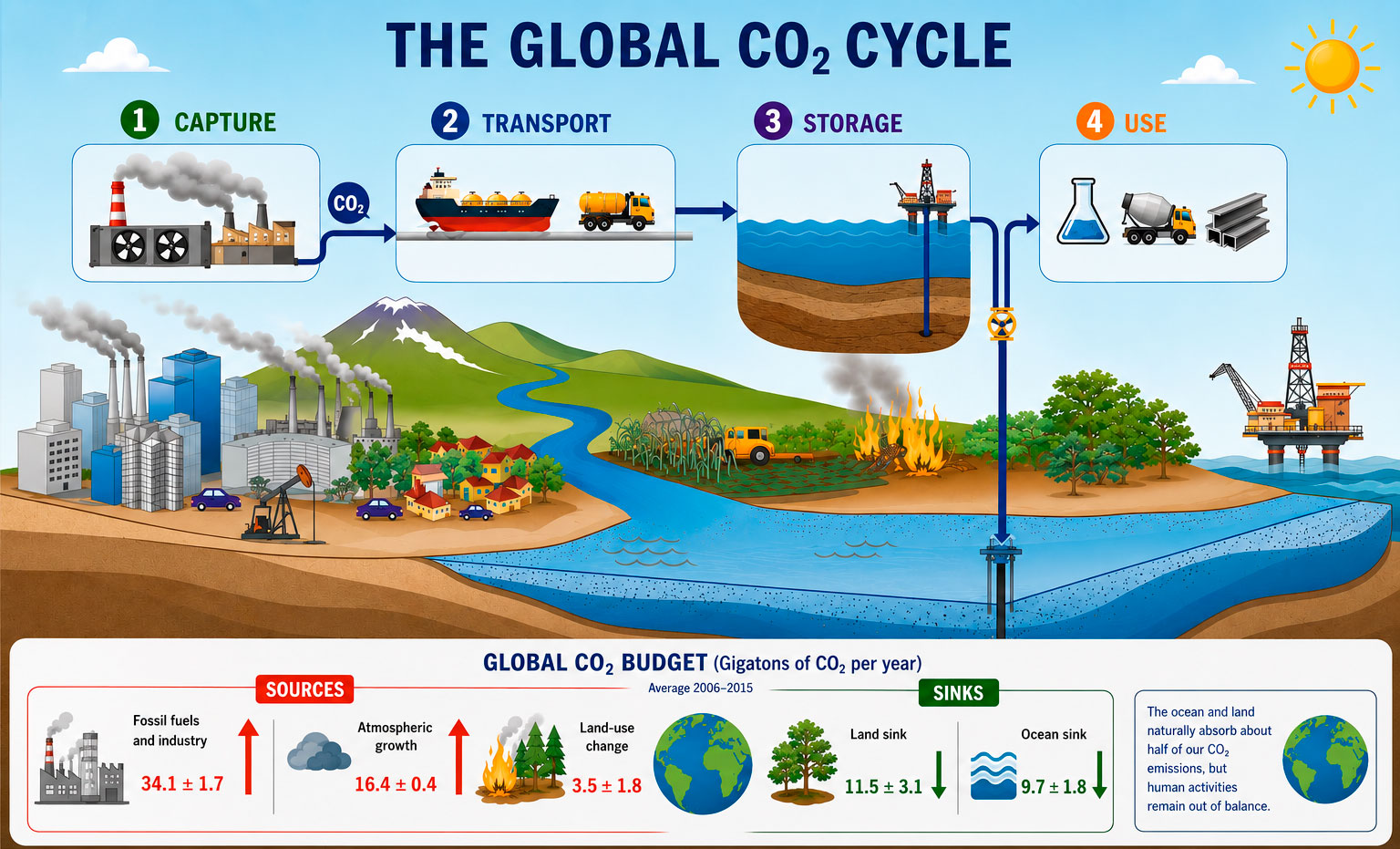

Europe’s path to climate neutrality by 2050 is entering a decisive phase. While renewables continue to expand, policymakers are increasingly relying on a less visible – but highly strategic technology: carbon capture, utilisation and storage (CCS/CCUS). The idea is straightforward. Capture CO₂ at industrial sites, transport it, and store it underground – or reuse it in industrial processes.

But behind this concept lies a far more complex reality. CCS is expensive, infrastructure-heavy and politically sensitive. And yet, without it, key sectors of Europe’s economy may struggle to decarbonise at all.

The European Commission has placed carbon capture firmly at the centre of its long-term climate planning. By 2030, the EU aims to build at least 50 million tonnes of annual CO₂ storage capacity. This could increase to around 280 million tonnes by 2040 and reach approximately 450 million tonnes by 2050.

These targets are closely linked to the EU’s proposed goal of reducing greenhouse gas emissions by 90% by 2040 compared to 1990 levels. CCS is expected to play a key role in achieving this reduction, particularly in sectors where emissions are difficult to eliminate through electrification alone.

Experts stress that carbon capture is not a silver bullet but indispensable for hard-to-abate industries like cement and steel. Without CCS, the cost of reaching net zero would be significantly higher. “With the world suffering the impacts of a worsening climate crisis, continuing with business as usual is neither socially nor environmentally responsible,” says Fatih Birol, Executive Director of the International Energy Agency.

At present, however, CCS remains a relatively small part of Europe’s overall emissions picture. Even the projected 450 million tonnes by 2050 would represent only a fraction of today’s total emissions. This underlines its role as a complementary technology rather than a primary solution.

From pilot projects to industrial scale

Across Europe, CCS is beginning to move beyond the demonstration phase. Several flagship projects are now under construction or entering operation.

In Norway, Northern Lights has become one of Europe’s most advanced carbon storage initiatives. The project, backed by Equinor, TotalEnergies and Shell, began its first CO₂ injection in August 2025. Its initial capacity is 1.5 million tonnes per year, with plans to expand to over 5 million tonnes annually by 2028.

Denmark is following a similar path with Project Greensand. The project aims to store CO₂ in depleted North Sea oil and gas fields. Commercial operations are expected to begin around 2026, with long-term capacity potentially reaching up to 8 million tonnes per year by 2030.

In the Netherlands, Porthos is under construction in the port of Rotterdam. The project is designed to capture CO₂ from industrial plants and transport it to offshore storage sites beneath the North Sea, with an annual storage capacity of around 2.5 million tonnes. However, following a schedule review, the start of operations has been postponed from the end of 2026 to the second half of 2027, partly due to the complexity of the project, interdependence between infrastructure components and longer delivery times for materials.

Southern Europe is also entering the CCS landscape. Greece’s APOLLOCO2 project is focused on building CO₂ transport infrastructure and has secured €169.3 million from the EU Innovation Fund.

Together, these projects illustrate a shift: CCS is moving from experimental technology to industrial infrastructure. However, the scale remains limited compared to what will be required over the coming decades.

A fast-growing market – with high costs

The financial dimension of CCS is both its greatest driver and its biggest obstacle. According to industry estimates, the European CCS market was valued at around $1.2 billion in 2024, with projected annual growth of approximately 24% through 2034.

At the same time, costs remain high. Capturing, transporting and storing CO₂ typically costs between €70 and €250 per tonne, depending on the sector, transport distance and storage method, although many large-scale projects aim to remain below €120 per tonne through shared infrastructure and economies of scale. For energy-intensive industries, this represents a significant additional expense without strong policy support.

“CCS deployment needs ‘regulatory certainty and stability to support investment,’” says Samantha McCulloch, Chief Executive of Australian Energy Producers, echoing broader IEA analysis on the importance of stable policy frameworks for large-scale carbon capture investment.

Economic viability also depends heavily on carbon prices under the EU Emissions Trading System. EU ETS prices fluctuated roughly between €60 and €100 per tonne in recent years, reaching average levels close to €90 per tonne during parts of 2023 and 2024.

This creates a structural challenge. If carbon prices fall, CCS investments become less attractive. If they rise sharply, industries face higher compliance costs, potentially affecting European competitiveness.

Global CO₂ Cycle Overview, Graphic by Energy Europe Editorial Team

Billions in public support

The European Union is backing CCS with substantial financial support. The EU Innovation Fund is expected to mobilise around €40 billion for low-carbon technologies between 2020 and 2030, with roughly €12 billion already awarded to projects across Europe. Additional support comes from the Connecting Europe Facility and the Just Transition Fund, both of which help finance infrastructure and industrial decarbonisation projects.

The European Union Emissions Trading System also creates a direct economic incentive for carbon capture. Companies that permanently capture and store CO₂ are exempt from surrendering emission allowances for those emissions, improving the financial viability of CCS projects.

In February 2024, the European Commission presented its Industrial Carbon Management Strategy, aimed at creating a more unified framework for CCS deployment across Europe. The strategy focuses on scaling CO₂ transport and storage infrastructure, harmonising regulation and attracting private investment.

However, the infrastructure challenge remains enormous. According to estimates by the European Commission’s Joint Research Centre, building a European CO₂ transport and storage network could require investments of roughly €10-20 billion or more over the next two decades.

Infrastructure and regulatory gaps

Beyond cost, infrastructure remains one of the biggest bottlenecks for CCS deployment in Europe. The continent still lacks a comprehensive network of CO₂ pipelines, shipping routes and certified storage sites capable of operating at large scale.

Cross-border coordination is therefore essential, as not all EU countries have suitable geological storage capacity. In practice, this means that captured CO₂ will often need to be transported across national borders – creating legal, regulatory and logistical challenges.

Regulatory fragmentation further complicates the picture. Differences in permitting procedures, liability rules and CO₂ accounting across member states can slow projects and increase costs for investors.

Kadri Simson has repeatedly stressed the importance of creating a unified European market for CO₂ transport and storage. Through its Industrial Carbon Management Strategy, the EU aims to establish a common framework that would accelerate CCS deployment, reduce infrastructure costs and improve investment certainty across the bloc.

A necessary tool – but not a solution on its own

Despite these challenges, most experts agree that CCS will play a necessary role in Europe’s energy transition. For sectors such as cement, steel and chemicals, where process emissions are difficult to eliminate, carbon capture may be the only viable option in the short to medium term.

However, its role will remain limited. Even under optimistic scenarios, CCS will complement – not replace – renewables, electrification and energy efficiency.

The coming decade will determine whether Europe can scale CCS fast enough to meet its climate targets. Success will depend on three factors: stable policy frameworks, large-scale investment and public trust.

Europe has made its bet. The question now is not whether CCS will be used – but whether it can be deployed at the scale and speed required to make a real difference.