Europe is looking ahead: In a new strategy for small modular reactors, the EU is betting on innovation and technological sovereignty. SMRs are not only intended to pave the way for a climate-neutral future, but also to send a strong signal for a self-confident, competitive Europe.

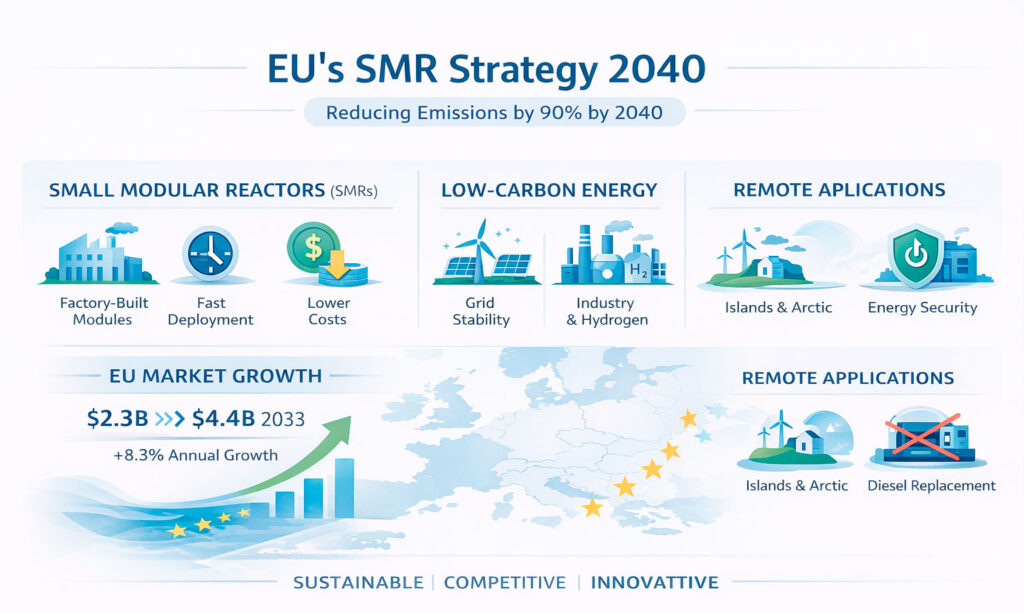

In March 2026, the European Union is set to unveil its strategy for developing and deploying small modular reactors (SMRs). This document will form part of the EU’s broader climate and industry agenda, which aims to reduce greenhouse gas emissions by 90% by 2040 compared to 1990 levels. SMRs are seen not only as a technological innovation in this context, but also as a building block of Europe’s future sustainable, low-carbon, industry-oriented energy architecture. For Brussels, the issue is not only about reducing emissions, but also about building a new industrial ecosystem that can ensure Europe remains competitive in the context of global technological change.

NUCLEAR SMR RENAISSANCE

Small modular reactors are more compact than conventional nuclear power plants. Their main difference is their modular design: key components can be manufactured in factories and then transported to the deployment site. This enables series production and could lower costs over time. Supporters argue that standardised designs can shorten construction timelines and make investments more predictable – a point that is especially relevant for first-of-a-kind projects in countries without experience building nuclear power plants.

Globally, nuclear power already avoids around 2 billion tonnes of CO₂ emissions per year while providing stable electricity generation. As the share of variable renewables such as wind and solar rises across the EU, the need grows for sources that can support grid stability and provide firm power. In that context, SMRs are presented as a complement to renewables that could reduce the need for gas-backed reserves and lower dependence on imported fossil fuels.

A further potential advantage is siting flexibility. In principle, SMRs could be located close to where energy is needed most – for example near steel production, hydrogen facilities, or industrial parks for battery manufacturing – supplying stable, low-carbon power directly. For energy-intensive industries, that could mean reduced exposure to price volatility and an easier path to decarbonising value and supply chains.

Beyond electricity generation, SMRs are often described as hybrid energy systems. They could help stabilise grids with a high renewables share, provide industrial heat for sectors such as chemicals, metallurgy, and cement, produce low-carbon hydrogen, and support district heating. Given the decarbonisation challenge in hard-to-abate sectors – including heavy industry and parts of transport – this flexibility is one reason SMRs are seen by advocates as a potential element of a broader energy transition.

EUROPEAN MARKET MOMENTUM

The European market for small modular reactors is estimated to be worth $2.29 billion in 2024. It is forecast to reach $2.48 billion in 2025, growing to $4.45 billion by 2033. This represents a compound annual growth rate of around 8.33% from 2025 to 2033. This growth is driven by the accelerated energy transition, rising electricity demand, and the need for low-carbon baseload power generation. Government commitments to achieving net-zero emissions and concerns about energy security are fuelling interest in new nuclear technologies.

Several European countries are actively considering SMRs as part of their long-term energy strategy. Poland is playing a leading role in this process by pursuing a policy of gradually phasing out coal and expanding nuclear energy. Europe’s first small modular nuclear power plant is under construction there. Additionally, countries such as Belgium, the Czech Republic, Finland, Italy, Lithuania, the Netherlands, Norway, Poland and Romania are exploring options for introducing small modular reactors, which could create a potential domestic market for European manufacturers.

The autonomous SMR segment is of particular interest. According to forecasts, it will experience the highest average annual growth rate of around 22.1% between 2025 and 2033. This rapid growth is driven by the need to ensure energy security in remote regions and at critical infrastructure facilities. Many islands and northern regions still rely on diesel generators, resulting in high operating costs and significant environmental impacts. Autonomous SMRs can provide a stable energy supply with near-zero emissions and long intervals between fuel changes, making them ideal for areas with logistical constraints.

A ROADMAP FOR THE EUROPEAN MARKET

According to the draft strategy, the European Commission views SMRs as a means of strengthening energy autonomy and fostering the growth of new industries. The aim is to establish a fully fledged European market for small reactors, with the first plants expected to be operational in the 2030s. The strategy emphasises that clearly defined demand, attractive conditions for investors, and timely commissioning of the first plants are crucial to developing a European SMR market.

Particular attention is paid to standardisation, series production, and the coordination of SMR licensing at the EU level. The plan is to establish European supply chains for components, as well as coordinating research, fuel issues and waste disposal for small reactors. After a long period during which no new nuclear power plants were built, issues such as securing expertise, training and further education for skilled personnel, and industrial cooperation are once again coming to the fore.

In the financial sector, mechanisms to mitigate investment risks for initial projects, state guarantees, and the utilisation of Europe-wide industrial support instruments are under review. Under the Euratom programme, €30 million has already been allocated to SMR safety research, and a further €15 million has been earmarked in the 2026-2027 work programme. These measures are intended to help establish a technological foundation and bolster investor confidence in this emerging industry.

SMALL REACTORS IN THE RACE TO NET ZERO

The European Commission’s new climate plans aim to reduce dependence on fossil fuels by 80% by 2040 compared to 2021 levels. In this context, Brussels recognizes the potential contribution of small modular reactors to achieving the energy and climate goals of the European Green Deal.

“We have decided to establish an industrial alliance for small modular reactors to facilitate the introduction of the first reactors by 2030 in countries that wish to do so,” explained Kadri Simson, then EU Commissioner for Energy, in 2024. She assured that the highest standards of safety and sustainable development would be maintained.

Thanks to their size, performance, and lower resource requirements compared to standard reactors, small modular reactors can ensure electricity grid stability in countries with high shares of renewables. In this respect, they serve as suitable replacements for thermal power plants running on fossil fuels like coal.

“The use of small modular reactors will bring significant benefits to Europe: greater energy independence, lower CO₂ emissions, new jobs, and economic growth,” explained Yves Desbazeille, Director of the European Atomic Forum (FORATOM).

GLOBAL CONTEXT AND OUTLOOK

Currently, there are more than 80 small modular reactor projects at various stages of development across 18 countries worldwide. Countries such as the USA, Canada, Japan and South Korea are actively promoting their own technologies, which is creating a competitive environment in the global market. According to forecasts by the International Energy Agency, small modular reactors could account for around 10% of global nuclear power capacity by 2040. Combined with a new wave of large-scale reactors, this could transform the global nuclear energy landscape. For Europe, this opens up the possibility of establishing nuclear energy as a key component of an environmentally friendly energy future, alongside the large-scale use of renewable energy sources, thereby strengthening the Union’s strategic autonomy.

GERMANY WEIGHS SMR OPTIONS

Berlin has repeatedly emphasised that there will be no return to decommissioned nuclear power plants. “We will not return to the old reactors,” declared German Economics Minister Katherina Reiche (CDU).

As far as SMRs are concerned, the ministry is already examining the possibility of joining countries actively developing these reactors. “We should examine new concepts, be part of the discussion and then decide,” said Reiche.

In Reiche’s view, Germany must phase out coal and gas – nuclear energy could provide a solution. She emphasised that it’s not about abandoning renewables, as solar and wind need base-load sources. SMRs are therefore viewed as a potential building block for Germany’s energy future.

ECONOMIC DIMENSIONS

The economic parameters of SMR projects vary considerably. Capital costs for a module are estimated at $1-7 billion. First-of-a-kind (FOAK) projects are more expensive due to planning and licensing, while future series production (NOAK) should achieve significant cost reductions through economies of scale.

No fixed total exists for a Europe-wide SMR program: financing depends on individual projects and countries, with EU support focusing primarily on research, coordination, and regulation. Europe is thus laying the foundation for a new technological direction that could become integral to its long-term energy strategy. If the first plants come online in the early 2030s, SMRs could secure their place in Europe’s model for low-carbon, industry-oriented growth.